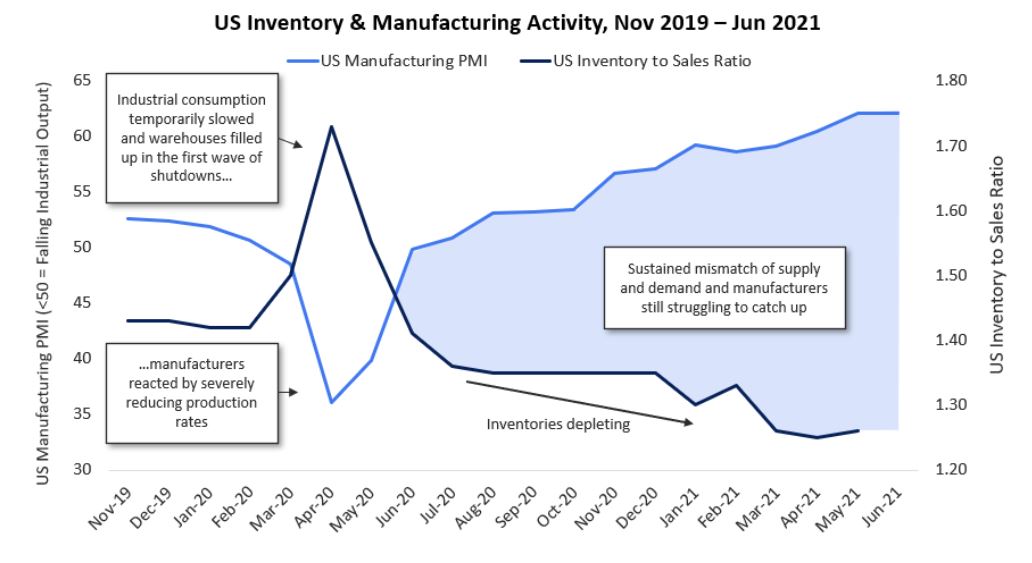

As global economies recover from the economic downturn, a combination of market forces is creating an inflationary cost environment for energy and natural resources firms. Severe shortages for key commodities, materials, and labor have businesses scrambling to mitigate the operational downsides, including longer lead times for critical equipment.

As US GDP growth, WTI prices and E&P activity continue their strong recovery, upstream operators have the opportunity to leverage CAPEX and OPEX forecasting to drive cost savings within an inflationary market.

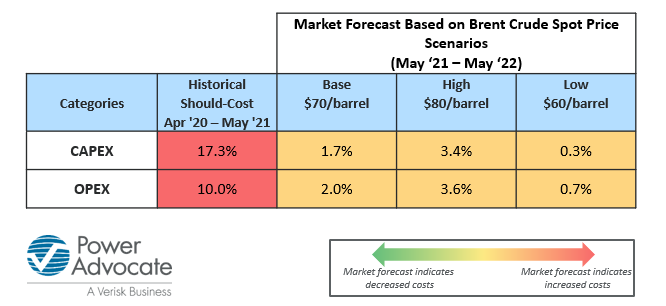

In our June report, we identify and provide cost forecasts for key CAPEX categories, including OCTG and drilling fluids and chemicals; and key OPEX categories, including compression services and well testing services. Operators are leveraging these forecasts to estimate key cost changes, forecast spend and use market data to optimise costs.

2021 marks an opportunity for upstream operators to overcome cost challenges presented amid last year's turbulent market through appropriate CAPEX and OPEX forecasting.

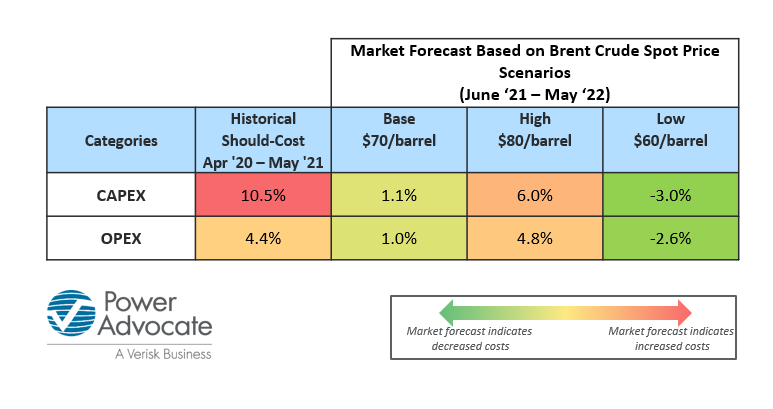

In our June update, we identify and provide cost forecasts for key CAPEX categories including OCTG, onshore & offshore drilling rigs; and OPEX categories including production chemicals and offshore support vessels.

In periods of rapid economic change, energy firms need to know where they are most vulnerable to rising costs. The recent volatility of commodity markets - and the uncertain fate of policies like President Biden's $1.2T infrastructure plan currently being debated in Congress - highlight the challenge that procurement teams face in estimating the expected impact on their budgets.

President Biden’s proposed $2T investment plan could strain an already tight labor market servicing utilities. As demand for various construction services increase, North American utilities will need to accomplish the same or greater levels of work compared to the past, but with a more constrained supply base. As a result, utilities must think about the potential higher costs that result from labor shortages.

Across the top areas of spend in the North American utility industry, our models reveal that costs for utilities have increased dramatically in the last year, upwards of 16%, and are forecasted to climb around 3% in a single quarter by the end of Q2 2021.

In our most recent whitepaper, we examine how supply chain professionals can confidently rise to the challenge by demonstrating they can offset the impact of inflation on an ongoing basis.

Volatile markets can have an adverse effect on operators, especially when having to purchase products and services off contract. For example, with Equipment Maintenance Services 8% off contract on average and costs expected to rebound c.3% by April 2022, operators must be prepared to manage their spend effectively to mitigate market changes.

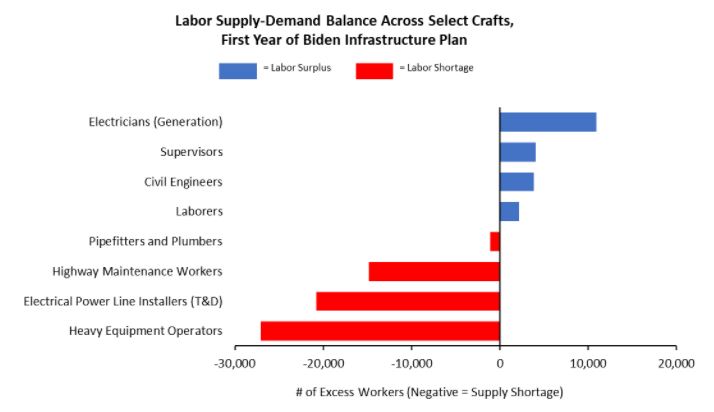

The US construction sector is facing a confluence of supply chain disruptions, cost increases, and worker shortages as the economic recovery from the pandemic accelerates. Now, President Biden’s proposed plan to invest $2T over 8 years in infrastructure could further boost demand for construction services, putting even more pressure on the limited labor supplies providing services to energy firms.

PowerAdvocate’s analysis of the proposed investments in roads, bridges, power transmission networks, and other physical infrastructure shows that higher demand will impact some craft labor types more than others. As the chart shows, demand is expected to exceed supply for several key crafts in the first year of the plan, with heavy equipment operators and electrical power line installers seeing the severest shortages. Both crafts saw minimal job losses in 2020 amid pandemic-related work stoppages and are currently near full capacity with few qualified workers remaining jobless. Meanwhile, both will see significantly higher demand if the infrastructure bill passes Congress. At a national level, PowerAdvocate forecasts that construction sector employers could face a shortage of 27,000 heavy equipment operators, or nearly 7% of the currently employed labor force of 405,000. For electrical power line installers, we forecast a shortage of 21,000 workers, or 18% of the current labor force of 114,000.

Labor shortages are a major risk for energy firms, impacting everything from costs, to safety, to project continuity. PowerAdvocate works with firms to quantify their exposure to these shortages and execute key supply chain strategies to mitigate the risk, including managing demand, improving supplier productivity, and enhancing volume commitments.

2021 marks an opportunity for upstream operators to overcome cost challenges presented amid last year's turbulent market through appropriate CapEx and OpEx forecasting.

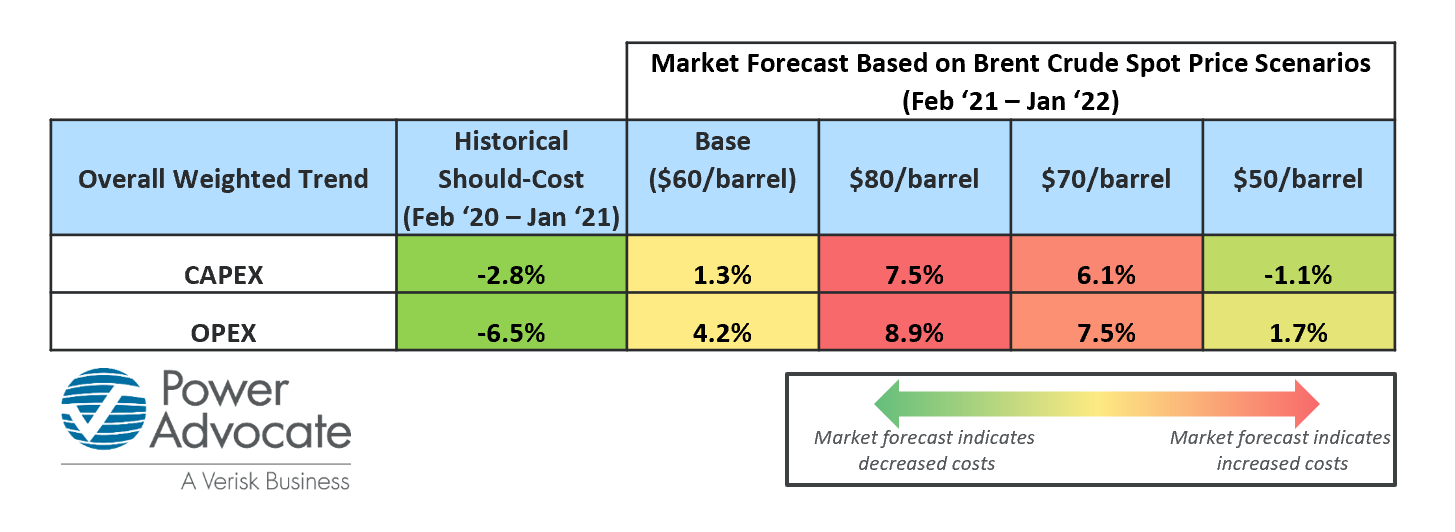

In our latest market report, we provide cost forecasts for key CapEx & OpEx categories and outline why we see cost increases across almost all of them which are forecast to rise between ~1%-12% between February 2021 and January 2022.

Some of the top categories with notable inflationary/deflationary trends included in the report are:

- CapEx: OCTG, onshore & offshore drilling rigs, and wellhead equipment services

- OpEx: Production chemicals, compression services, and offshore support vessels

As operators focus on optimizing their costs in 2021, it is key to leverage market forecasts to estimate key cost changes and forecast spend.

Market Forecast Overall Weighted Trend Based on Brent Crude Spot Price Scenarios

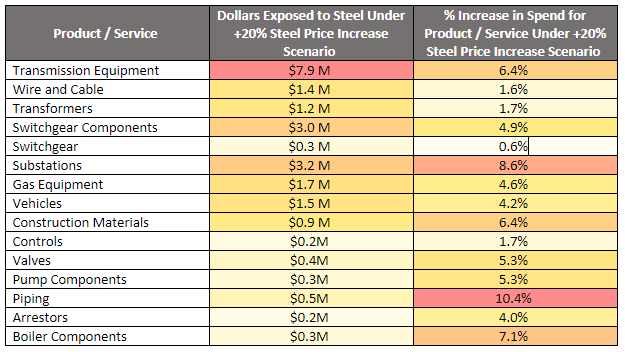

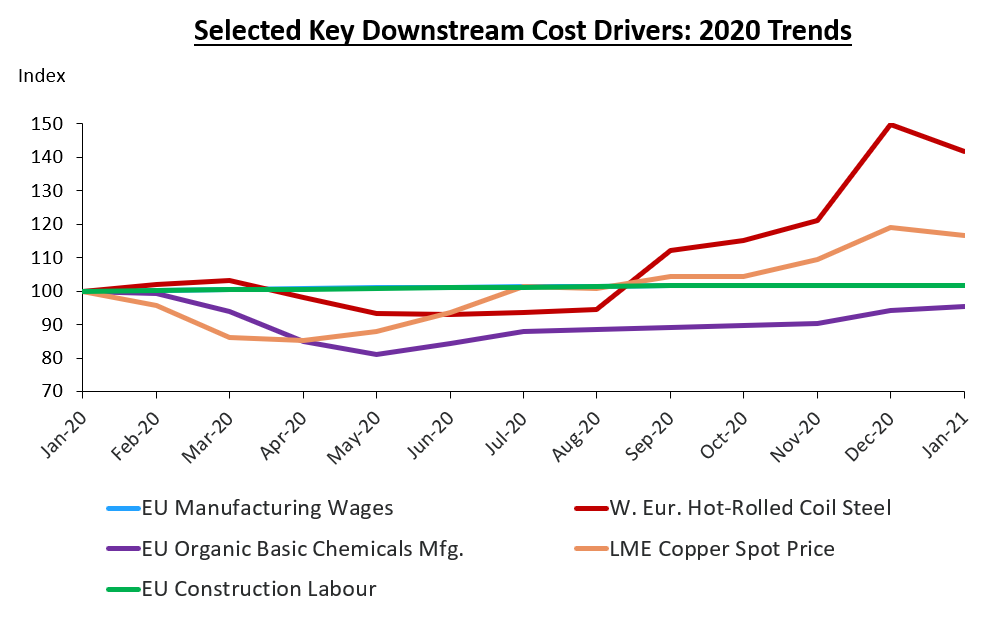

2020 has been a volatile year for downstream supply markets, and several key cost categories have moved sharply. For example, since last January,

- Hot-Rolled Coil Steel costs have increased by 40%+

- Copper costs have increased by 16%+

- Organic Basic Chemicals costs have decreased by 4%+

As operators refine their CapEx and OpEx programs for 2021, we have found that it is important to understand both how key downstream commodities have trended, and the impacts of those trends on key cost categories – for example, the 16%+ increase in copper costs contributed to a 7%+ increase in Electrical Supplies.