As E&P companies hustle to react to the drop in oil prices, we’ve seen many customers pursue a 'give me 20% (or some other number decided by management) off' strategy to driving cost reduction through suppliers. The CEO of NOV recently said that “it seems [customers] are sending everyone the same form letter demanding double digit price concessions."

For decades, PowerAdvocate has helped energy companies drive savings through supply chain via better data and intelligence, and we know that a more thoughtful and fact-based approach to generating savings can yield significantly better results.

In this post, we lay out 3 reasons why a strategy of pursuing 20% (or 10% or 30%) savings from suppliers across the board is a suboptimal one. In the ‘Smart Savings Series’ that follows, we will dive deeper and provide specific recommendations on where to look and how to find outsized savings opportunities across your supply base by using spend data, market intelligence and cost models. Our goal is to help E&P supply chain organizations get smart about where and how to pursue savings through better data.

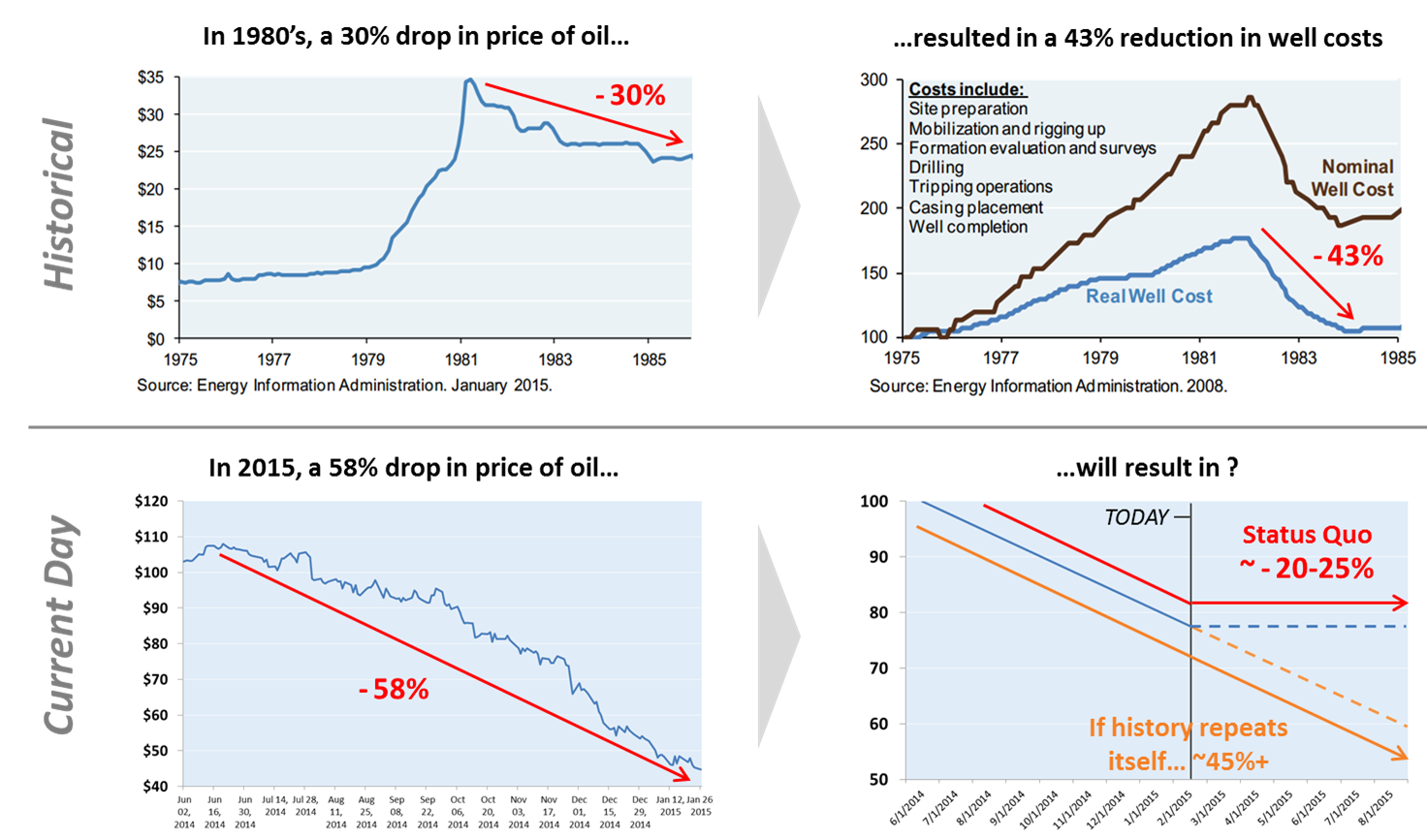

1. Historically, E&P Companies Have Achieved Far More than 20% Savings Following Large Dips in Oil Prices

In the past, E&P companies have demonstrated the ability to drive massive cost reductions through supply chain when prices experience a significant drop. For example, from the period 1975-1982, well costs increased by 75%. When oil prices tanked in 1982, that entire gain was reversed in less than two years, implying a 'savings' number of 43%.

And to think that in that period, oil prices dropped just 26%. Compare that with the recent dip of 55% from its peak, and you should begin to believe that there is significantly more savings out there than the 20% your team may be pursuing. For example, JP Morgan predicts a reduction of 35% in costs of fracking sands, and 30% in day rates for land drilling rigs.

2. Some Materials are More Impacted by Dips in Commodity Prices and Demand than Others

In the last 8 months, historic shifts in commodity markets have created unprecedented savings opportunities for E&P companies...but what materials have been most directly impacted?

Knowing which cost drivers have moved and the relative impact of those movements, and knowing which suppliers have the most excess capacity (and therefore margin to give) enables a highly focused, effective effort to drive down enterprise costs.

For example, did you know that 25% of your suppliers OCTG casing costs is comprised of steel? So when steel prices move, as they have in the past 6 months, do you know what impact that should have on your costs? If not, you should!

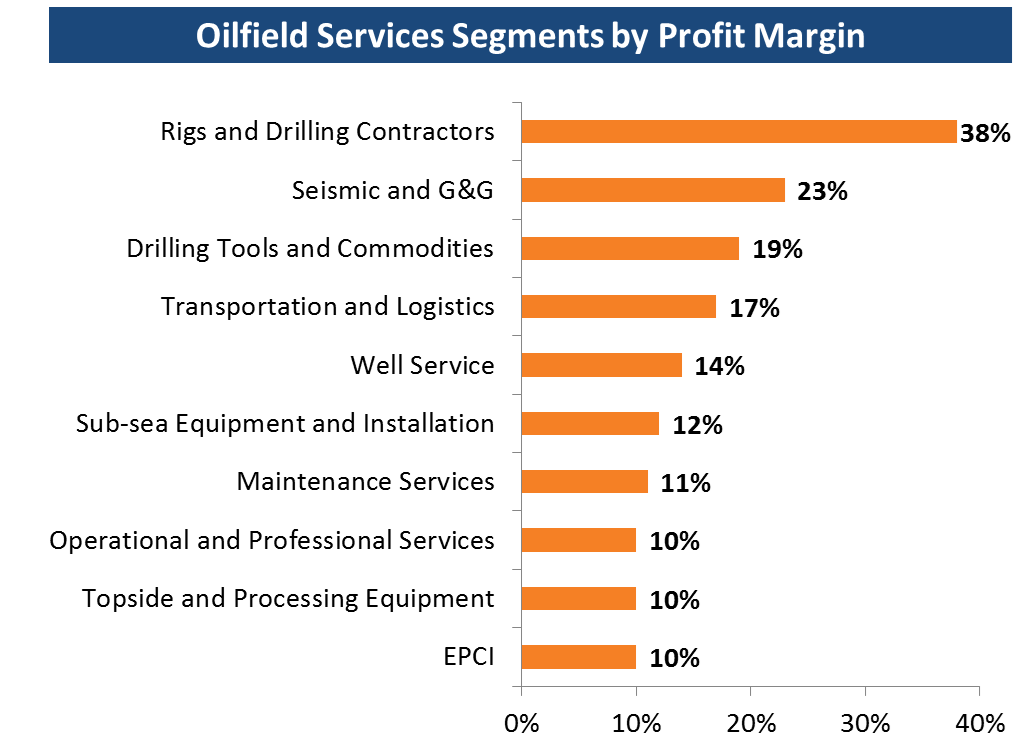

3. Suppliers have Different Margin to Work With for Different Services

Demanding “blanket” savings percentages may be simple and convenient for supply chain, but results will be varied because this approach does not reflect the reality of your suppliers' businesses. Different materials and services have vastly different cost structures, levels of competition, and thus margin. Therefore, knowing how much room a specific supplier likely has to give is critical to informing a productive negotiation with that supplier and extracting an appropriate amount of savings from them.